With interest rates fluctuating and lending policies evolving, securing the best mortgage rates in 2026 requires smart planning and informed decisions. Whether you’re a first-time homebuyer or an investor, understanding how lenders evaluate borrowers can help you save lakhs over the life of your loan. This guide is aligned with the most searched financing-related queries to help you make the right moves.

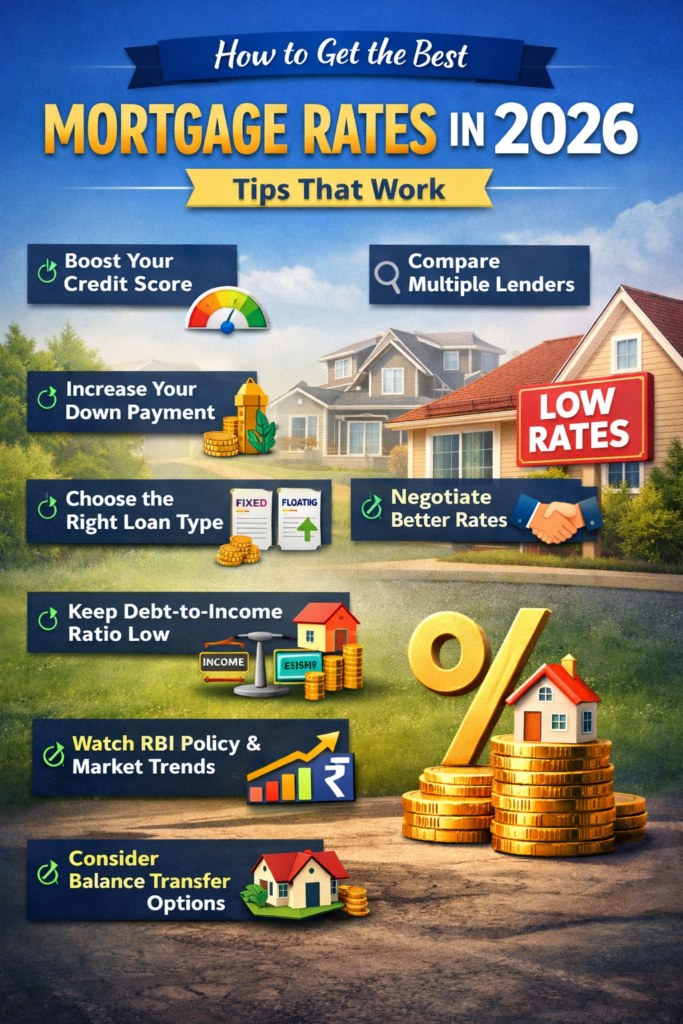

1. Maintain a Strong Credit Score

Your credit score remains the most important factor affecting mortgage rates in 2026. Lenders typically offer their lowest rates to borrowers with scores above 750.

Actionable Tips:

- Pay EMIs and credit card bills on time

- Keep credit utilization below 30%

- Avoid multiple loan or credit card applications before applying for a mortgage

2. Compare Mortgage Rates from Multiple Lenders

Never settle for the first offer. Mortgage rates vary across banks, housing finance companies, and NBFCs.

Why it matters:

Even a 0.25% lower interest rate can save you a significant amount over a 20–30 year loan tenure.

Search-aligned keywords:

- best home loan interest rates 2026

- compare mortgage rates India

3. Choose the Right Loan Type

In 2026, borrowers can choose between fixed-rate, floating-rate, and hybrid loans.

- Fixed-rate loans: Stable EMIs, higher initial rates

- Floating-rate loans: Lower rates, affected by RBI policy changes

- Hybrid loans: Fixed for initial years, then floating

Tip: If interest rates are expected to fall, floating rates may be more cost-effective.

4. Increase Your Down Payment

A higher down payment reduces the lender’s risk and can help you secure lower mortgage interest rates.

Ideal approach:

- Aim for 20–30% down payment

- Lower loan-to-value (LTV) ratio = better interest rate offers

5. Keep Your Debt-to-Income Ratio Low

Lenders in 2026 prefer borrowers whose total EMIs do not exceed 40–50% of monthly income.

How to improve it:

- Close high-interest personal loans

- Avoid new debts before mortgage approval

6. Opt for Shorter Loan Tenures

Shorter tenures often come with lower interest rates and significantly reduce total interest paid.

Example:

A 20-year loan may have a lower rate than a 30-year loan, even though EMIs are slightly higher.

7. Negotiate with Lenders

Many borrowers overlook negotiation. If you have:

- A strong credit profile

- Stable income

- Existing relationship with the bank

You can often negotiate better mortgage terms and interest rates.

8. Monitor RBI Policy & Market Trends

Mortgage rates in India are closely tied to RBI repo rate changes. Staying informed helps you time your loan application better.

Search-aligned keywords:

- home loan interest rate forecast 2026

- RBI repo rate impact on home loans

9. Consider Balance Transfer Options

If you already have a home loan, balance transfer to another lender offering lower rates can reduce your EMI burden.

Ensure you calculate:

- Processing fees

- Legal and valuation costs

- Net savings over the remaining tenure

10. Keep Your Documentation Ready

Quick approvals often lead to better deals.

Essential documents:

- Income proof

- Bank statements

- Property documents

- Credit report

Final Thoughts

Getting the best mortgage rates in 2026 is about preparation, comparison, and timing. By improving your credit profile, choosing the right loan structure, and staying aware of market trends, you can secure a mortgage that fits your long-term financial goals.